Personal Finance Made Simple

Personal Finance: A Complete Guide

Understand your money, build better habits, and take control. Everything you need to know about personal finance.

Money skills anyone can learn

Personal finance doesn't require a degree in economics. At its core, it's about three things: knowing where your money goes, spending less than you earn, and putting the difference to work. That's it.

Most people struggle not because personal finance is complicated, but because they don't have a plan. A simple budget and an investment strategy - that's what makes the difference.

This guide breaks down everything you should know about managing your money.

Three things that actually matter

Liquidity

Going broke can often be a timing issue. A budget shows where your money goes, and an emergency fund keeps you afloat when life happens.

Investing

Don't pay management fees. Low-cost index funds beat most active managers. Build a simple portfolio, automate it, and let compound growth work.

Stability

Don't let debt or disaster wipe you out. Kill high-interest debt first, get essential insurance coverage, and protect the wealth you've built.

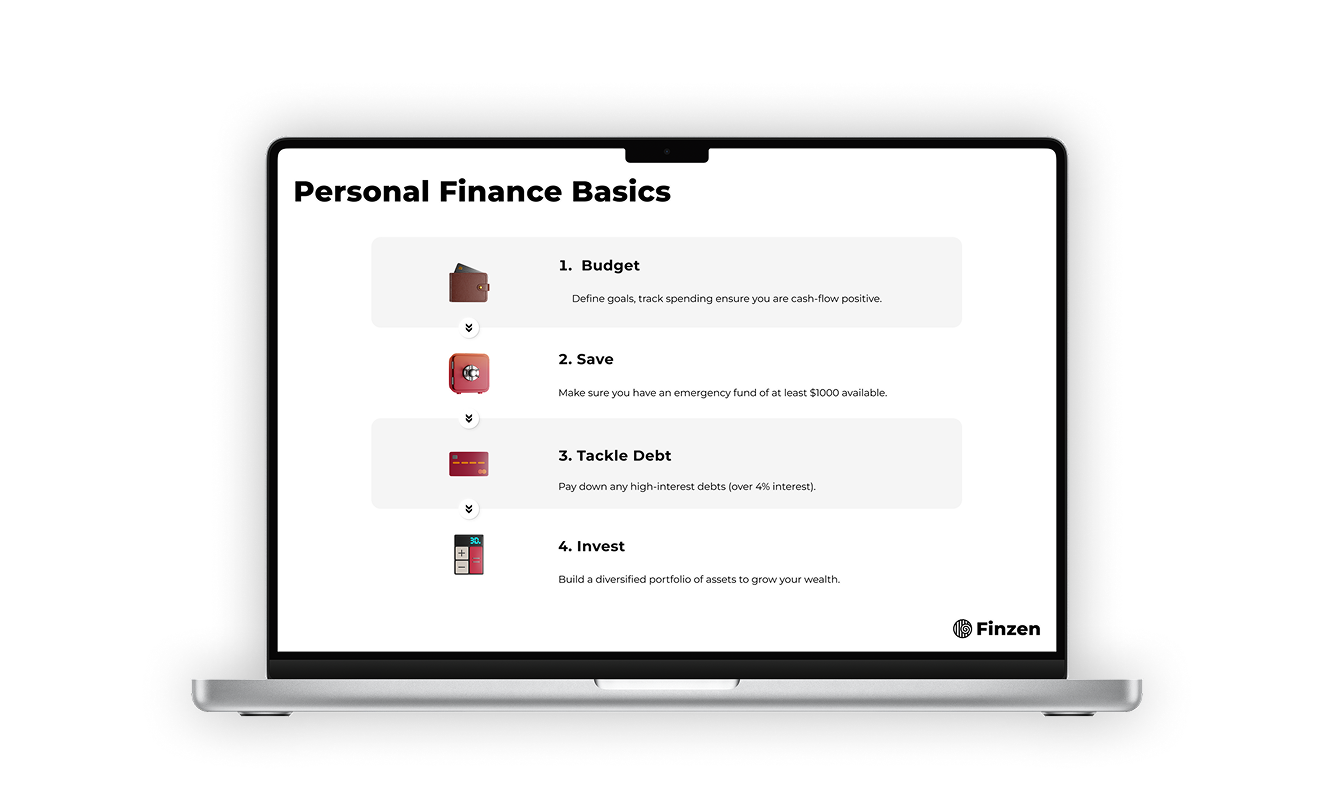

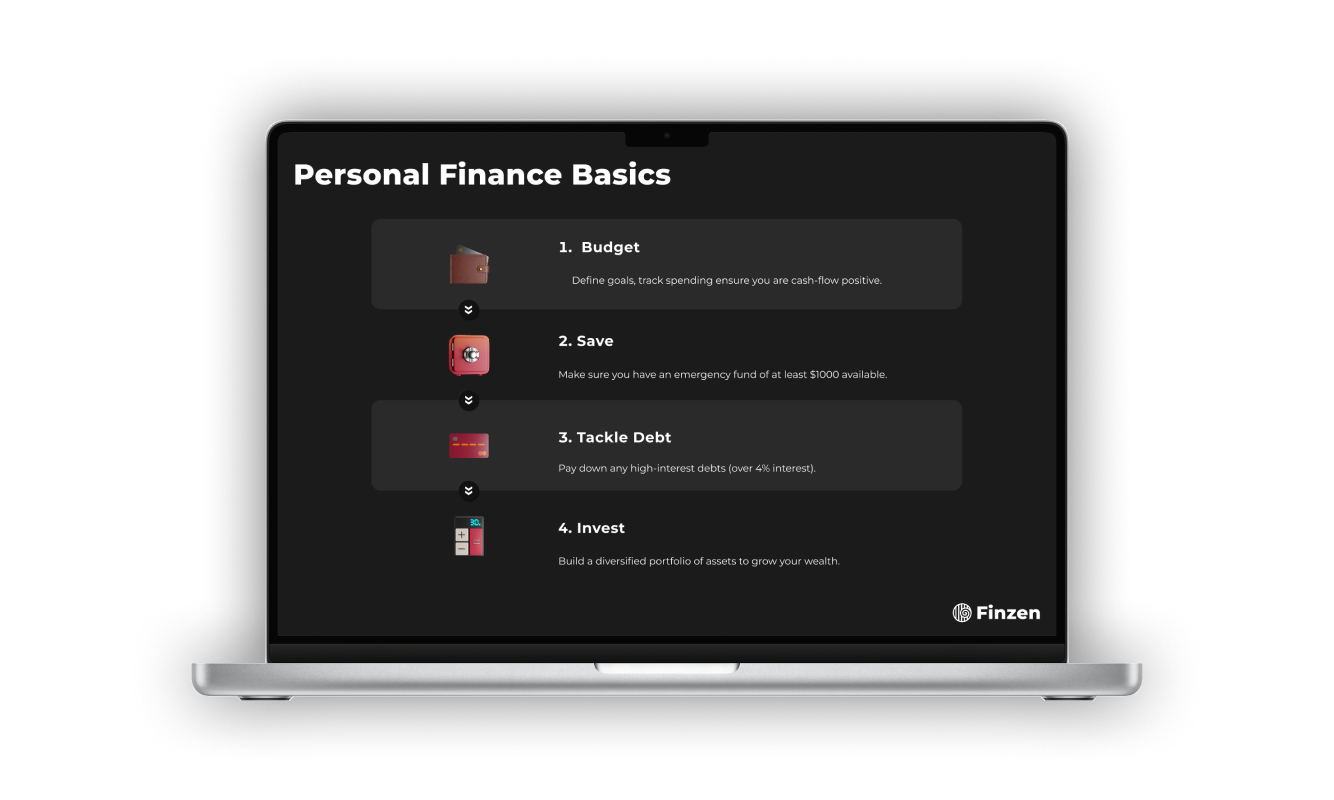

The personal finance to-do list

How many of these have you covered?

1. Set up a budget tracking system

Choose an app or spreadsheet to track expenses. Start logging where your money goes.

2. Build your emergency fund

Save 3 months of expenses in a high-yield savings account. This is your financial safety net.

3. Pay down bad debts

Anything over 4% is considered high interest. Don't let it compound against you.

4. Build an investment portfolio

Invest excess capital in a diversified portfolio to grow wealth and combat inflation.

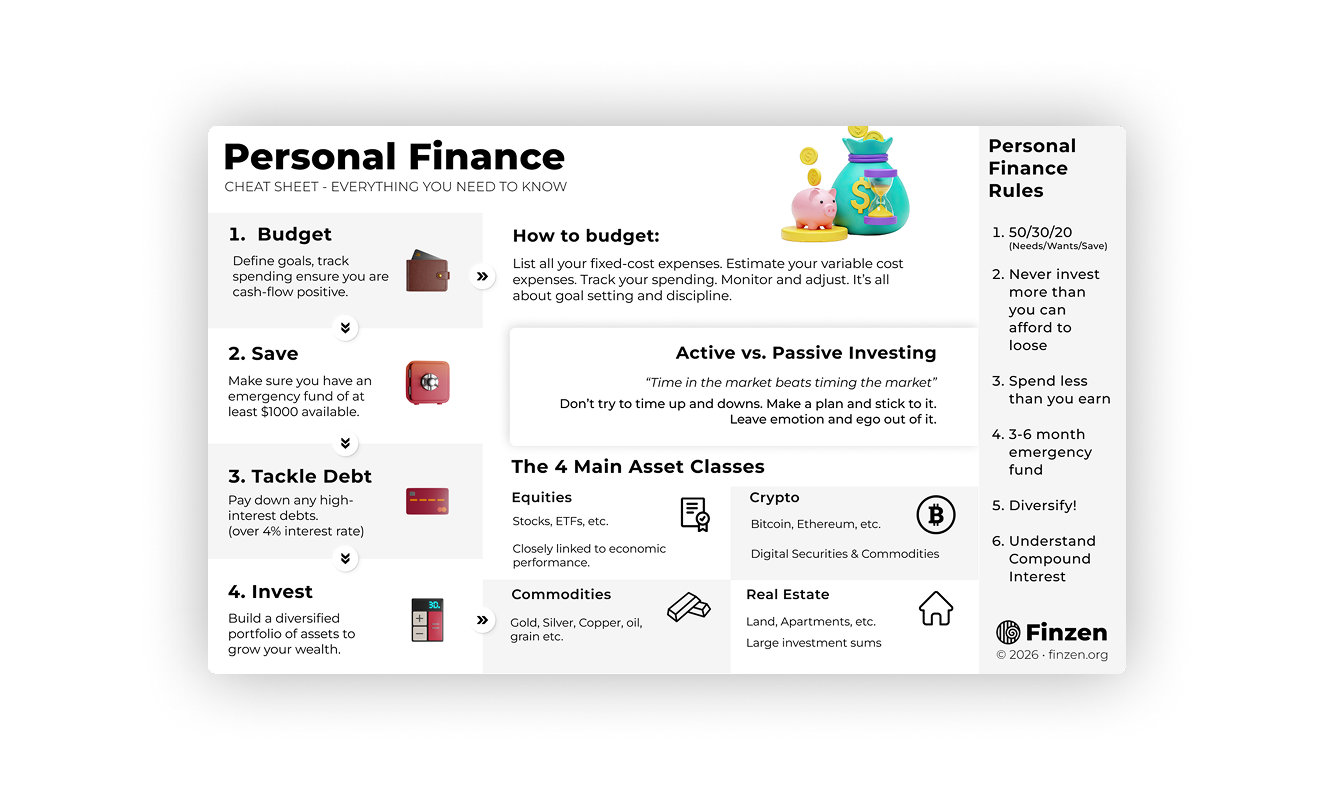

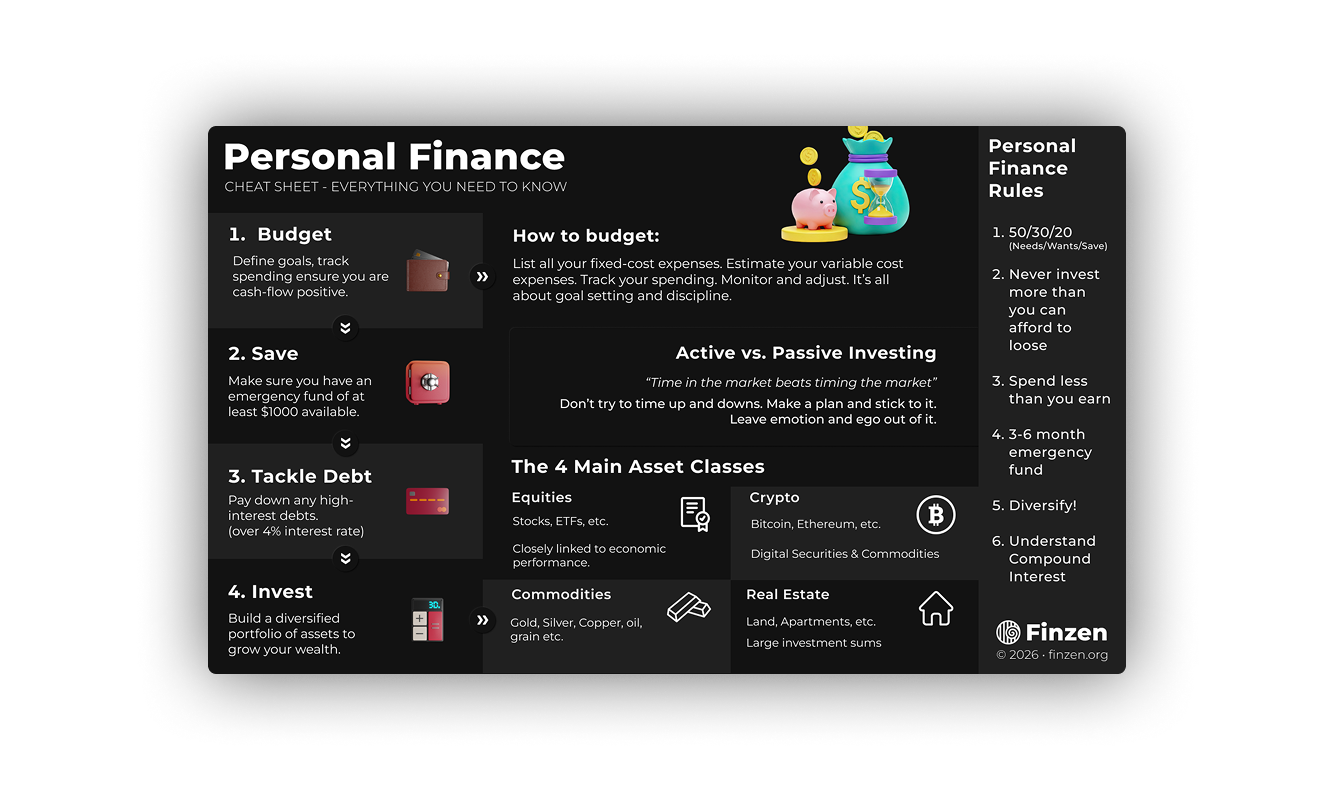

Budgeting made simple

A budget is just a written financial plan.

Write down your fixed costs, estimate variable costs. Track your spending, adjust your budget and take control of where your money goes.

Envelope based budgeting is one of the most popular budgeting methods. Imagine your spending categories as envelopes. At the beginning of the month you put in a certain amount of money, and when it's empty, no more spending for that category.

Liquidity

Why you need an emergency fund

Having money isn't enough - it needs to be liquid and available when you need it. Tracking your cashflow shows exactly how long your emergency fund will last. When you know your burn rate, you know your runway.

An emergency fund (3–6 months of expenses) protects: your ability to weather job loss, medical bills, or car repairs without selling investments at a bad time. Liquidity means options. No liquidity means forced decisions.

Investing

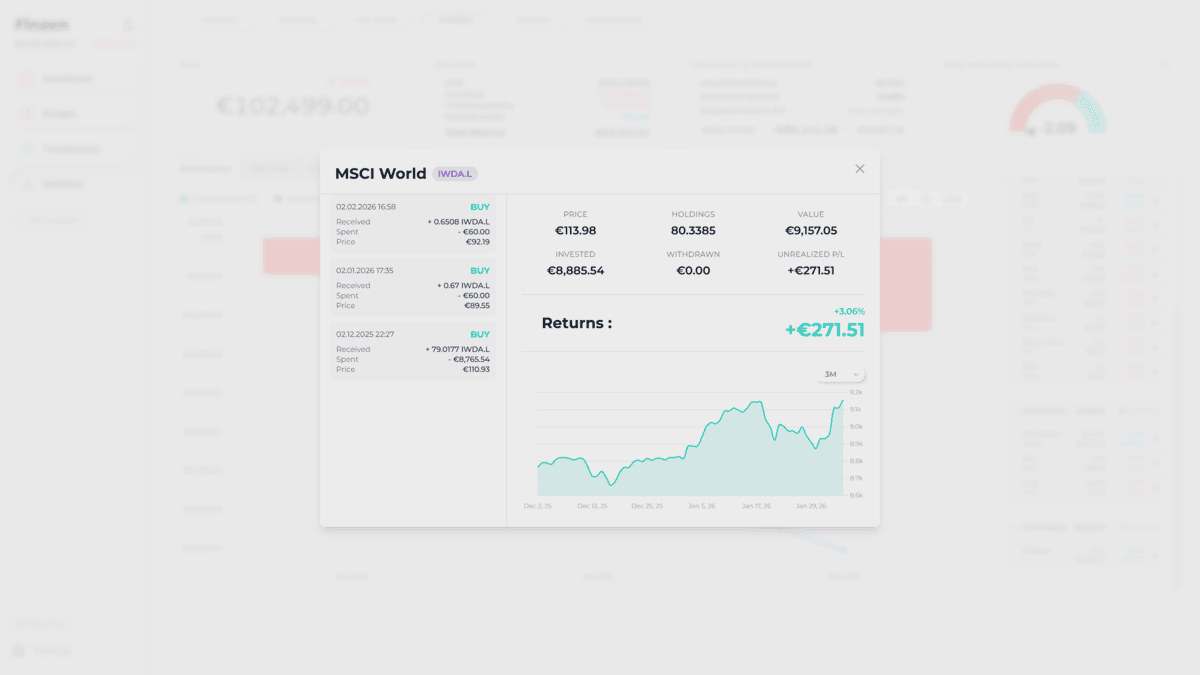

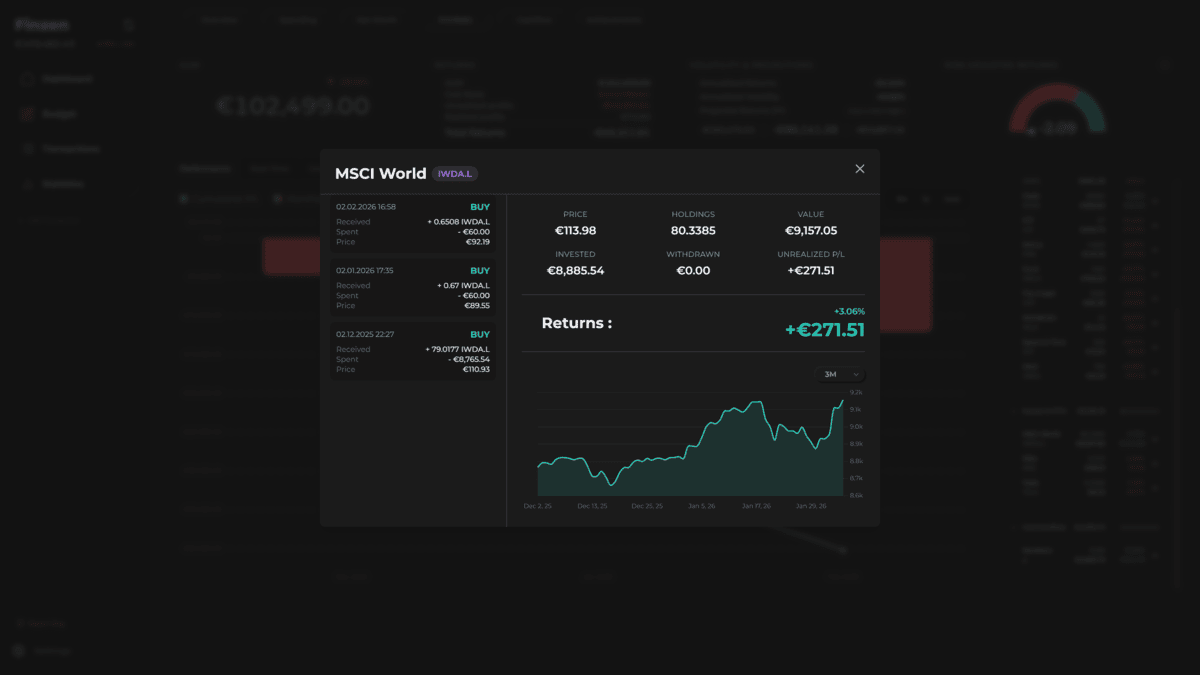

Asset allocation, diversification, and portfolio management

Diversify your portfolio: equities (stocks, ETFs, Mutual Funds,...), real estate, commodities, and crypto. Each carries different risk and return profiles. Most investors start with equities through index funds - broad exposure, low fees, proven track record (around 10% returns per year).

Active vs. passive investing: Active management (picking individual stocks) usually loses to passive strategies after fees. Diversification across assets and sectors reduces risk. Dollar-cost averaging (DCA) - investing the same amount regularly - removes timing decisions and emotion.

Track your portfolio. Monitor allocation, rebalance annually, understand what you own. Never invest more than you can afford to lose. Risk tolerance isn't theoretical - it's what lets you sleep at night when markets drop 20%.

Just start and you'll already be ahead of most

of Americans experience "significant" stress over money

of households have a written financial plan

of Americans spend more than they earn

Financial literacy isn't taught in schools. Most people learn money management through trial and error. But to be fair doing anything is better than doing nothing. So just start!

The good news: you don't need to master everything. You just need a few key principles and a simple way to track your progress. That's exactly what Finzen provides.

Personal Finance Rules of Thumb

Master these personal finance rules and you'll avoid the mistakes that keep most people broke. They work at any income level.

-

Spend less than you earn

The foundation of all personal finance. If you consistently spend more than you make, no investment strategy or budget hack will save you. Track it, measure it, fix it.

-

50/30/20 budgeting rule

50% for needs (housing, food, utilities), 30% for wants (entertainment, dining out), 20% for savings and debt. It's a starting framework, adjust based on your situation.

-

Build an emergency fund

3-6 months of expenses in cash. Not invested. Not in crypto. Boring, accessible cash. This prevents life's inevitable surprises from becoming financial disasters.

-

Prioritize high-interest debt

Credit cards at 20% APR are emergencies. Paying minimums while investing is like plugging one hole while drilling another. Kill the expensive debt first.

-

Never invest more than you can afford to lose

Investments fluctuate. Markets crash. If losing the money would devastate you financially or emotionally, it shouldn't be invested. Emergency funds come before portfolios.

-

If it sounds too good to be true, it is

Guaranteed 50% returns. Zero-risk investments. Get-rich-quick schemes. They prey on hope and ignorance. Real investing is boring, slow, and proven - not exciting and miraculous.

-

DYOR — Do Your Own Research

Never invest in something you don't understand. Read the prospectus. Know what you own. If you can't explain it simply, you don't understand it well enough to risk money on it.

-

Time in the market beats timing the market

Trying to predict market tops and bottoms usually fails. Consistent investing over decades beats attempting perfect entry points. Start now, invest regularly, stay invested.

-

Compound interest & diversification

Einstein allegedly called compound interest the eighth wonder. Small amounts invested early grow exponentially. Diversification protects you when individual investments fail. Both are essential.

-

Don't keep up with the Joneses

Your neighbor's new car and exotic vacations? Probably financed by debt they can't afford. Comparing yourself to others' spending is how lifestyle creep happens. Live within your means, not theirs.

These aren't restrictions, they're guardrails. Follow them and you'll avoid most financial mistakes. Ignore them and you'll learn the expensive way why they exist.

It all starts with a plan

And making sure you stick to it

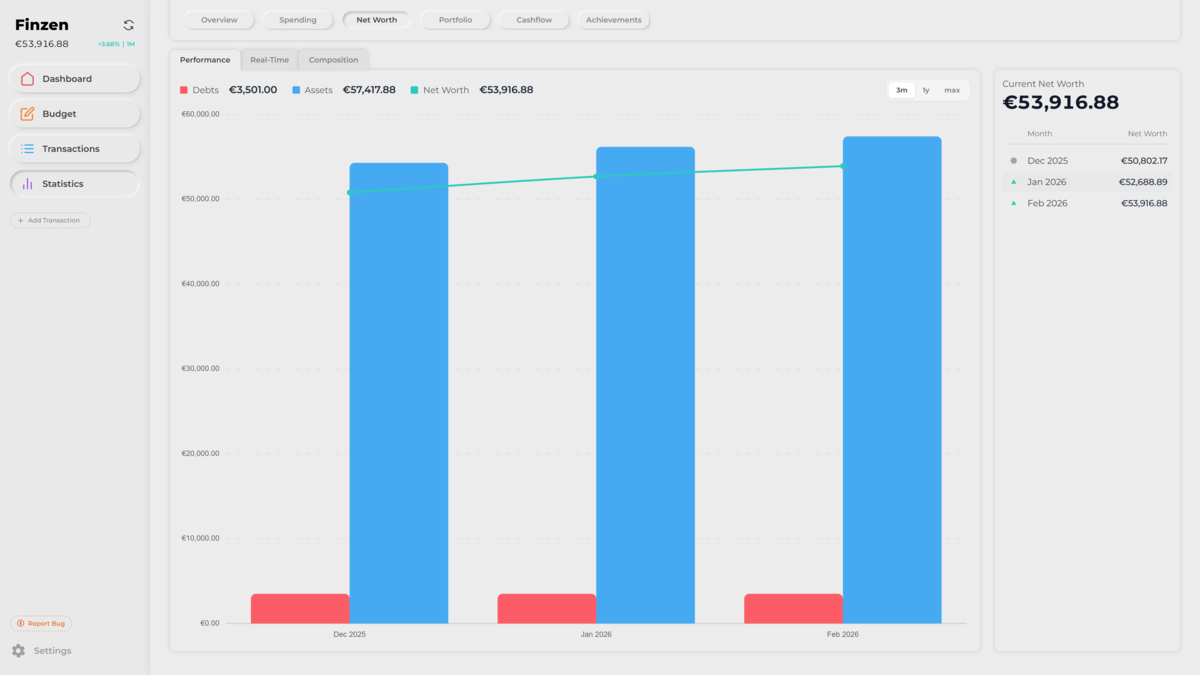

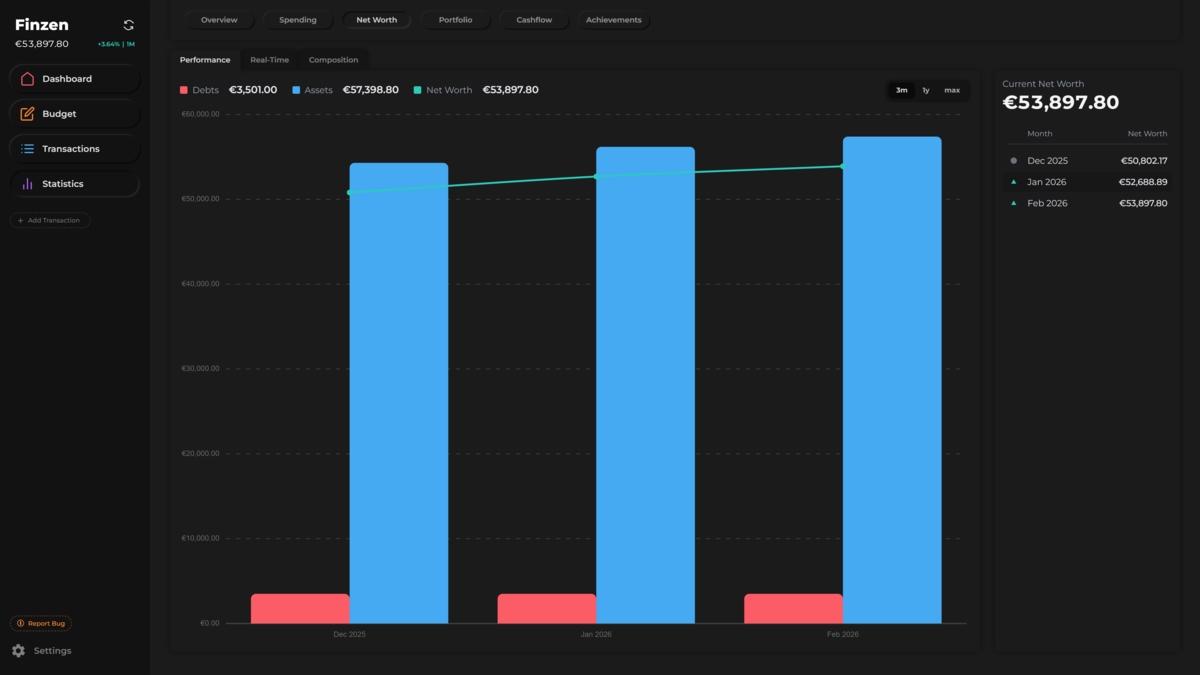

You've learned the fundamentals: budget your spending, build liquidity, eliminate high-interest debt, invest the surplus. But knowing isn't enough. A written financial plan transforms intentions into actions.

Daily tracking is what makes it stick. It takes 30 seconds to log a transaction. That small habit creates awareness, reveals patterns, and keeps you accountable.

Recap: Personal Finance Flowchart

How to prioritize your money. Do in order. Don't skip steps.

Track your spending

Before anything else, know where your money goes. You can't fix what you can't see. Even one week of tracking reveals surprising patterns. Make sure to spend less than you earn.

Build a starter emergency fund ($1,000)

A small cash buffer prevents minor emergencies from becoming credit card debt. This is your first savings goal - small but critical.

Pay off high-interest debt

Credit cards charging 20%+ APR are emergencies. Pay minimums on everything else, throw all extra money at the highest-rate debt. Repeat until gone.

Build a full emergency fund (3-6 months)

Now expand that buffer to cover 3-6 months of expenses. This protects you from job loss, medical issues, or major repairs without touching investments.

Invest for the future

With debt gone and emergencies covered, start investing. Build a portfolio diversified. Don't try to time the market - that's gambling. Consistency beats timing.

The key insight: This order exists because each step protects the next. An emergency fund prevents new debt. No debt means more money to invest. It's a sequence, not a checklist.

Common personal finance mistakes to avoid

Learn from what trips most people up

Too many categories

Starting with 30+ budget categories guarantees failure. Start with 5-8: Housing, Food, Transport, Utilities, Savings, Entertainment. Add more only when you actually need them.

All-or-nothing thinking

One overspend doesn't ruin everything. Budgets flex. Adjust and keep going. The goal is direction, not perfection. Quitting after a "bad" week is the real failure.

Forgetting irregular expenses

Car insurance, annual subscriptions, gifts, medical bills - they're predictable, just not monthly. Set aside a small amount each month for these "surprise" expenses that aren't actually surprises.

Unrealistic targets

Cutting dining out from $400 to $0 in one month? That's a recipe for failure. Cut to $300 first. Then $200 next month. Gradual, sustainable changes stick. Drastic cuts don't.

The pattern: most mistakes come from trying to do too much too fast. Start small. Be consistent. Adjust based on reality. That's the formula that works.

Your personal finance guide at a glance

Everything on this page, distilled into one visual. Print it, save it to your phone, or stick it on your fridge. The best financial plan is the one you actually remember.

Questions beginners ask

-

Start by tracking your spending for one week. Don't change anything yet, just write down every transaction. This reveals where your money actually goes, not where you think it goes. Once you see patterns, create 5-6 broad budget categories (housing, food, transport, entertainment, savings). Set realistic limits based on what you learned. The biggest beginner mistake is trying to track 30+ categories from day one. Start simple, add complexity only when you need it.

-

Living paycheck to paycheck usually means one of three things: you're spending more than you earn, you're not accounting for irregular expenses (insurance, gifts, annual subscriptions), or you lack visibility into where money actually goes. Small daily purchases add up invisibly - that $6 coffee becomes $180/month, $2,160/year.

Track every transaction for one month. Most people discover $200-400 in "leakage" they didn't realize existed. Then budget for irregular expenses by setting aside money monthly - if car insurance costs $600/year, save $50/month so it's not a surprise. Cash flow tracking shows exactly how long your money lasts and where the gaps are.

-

Don't invest until you have 3-6 months of expenses saved in an emergency fund. This isn't being conservative - it's preventing disaster. Without liquidity, the first emergency (car repair, medical bill, job loss) forces you to sell investments at the worst possible time or rack up high-interest credit card debt.

The order matters: build a starter emergency fund ($1,000), kill high-interest debt (anything over 6-8%), then complete your emergency fund, then invest. Investing while carrying 20% APR credit card debt is like filling a bathtub with the drain open. Track your net worth to see both emergency funds and investments grow together - they're different tools serving different purposes.

-

"Good" debt has three characteristics: low interest rate (under 4-6%), builds equity or income potential (mortgage, student loans for in-demand careers), and the asset typically appreciates or generates returns. "Bad" debt is high-interest (credit cards at 15-25%), used for depreciating assets (new cars, consumer goods), and drains your monthly cash flow.

The real test: can the thing you're borrowing for generate more value than the interest cost? A mortgage at 3.5% on a home that appreciates is mathematically sound. A credit card at 22% for clothes or dining out is financially destructive. Track your debts alongside your net worth - seeing the interest pile up monthly is a powerful motivator to eliminate it. Prioritize paying down anything over 6-8% before investing excess income.

-

Overspending happens when spending is invisible or emotional. The solution is friction and awareness. Use envelope budgeting - allocate fixed amounts to categories, and when the envelope is empty, you're done for the month. This forces conscious decisions: "Do I really want this, or do I want to save this budget for something better?"

Implement a 48-hour rule for non-essential purchases over $50. Write them down, wait two days, then decide. Most impulse purchases lose their appeal quickly. Manual transaction tracking (not automatic bank sync) creates natural friction - logging every purchase makes you confront spending patterns. When you have to write "$47 - impulse Amazon order" into your budget, you start questioning whether it was worth it.

-

Yes, if you want to actually understand your finances. The small stuff matters - it's not about the $3 coffee, it's about realizing you spent $90 this month on coffee without noticing. Untracked spending is invisible spending, and invisible spending is where budgets fail. You can't manage what you don't measure.

The good news: it takes 30 seconds per transaction. Log it when you spend it, not at the end of the week from memory. That daily ritual of recording transactions creates mindfulness - you become conscious of spending patterns instead of wondering where your money went. After 2-3 months, tracking becomes automatic habit, and your budget reflects reality instead of wishful thinking. Most people find $200-400/month in spending they didn't realize was happening.

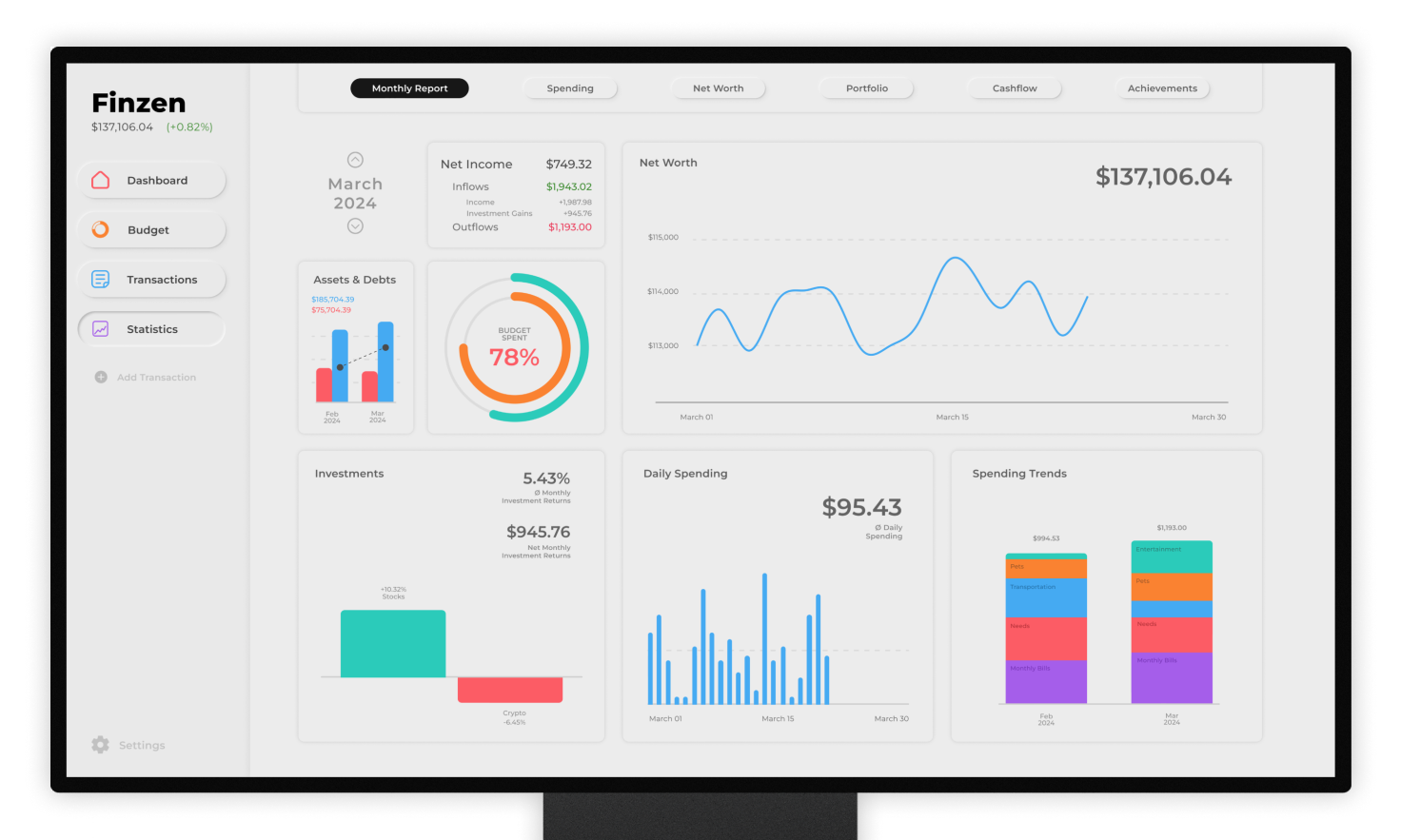

Finzen

The all-in-one personal finance tracker

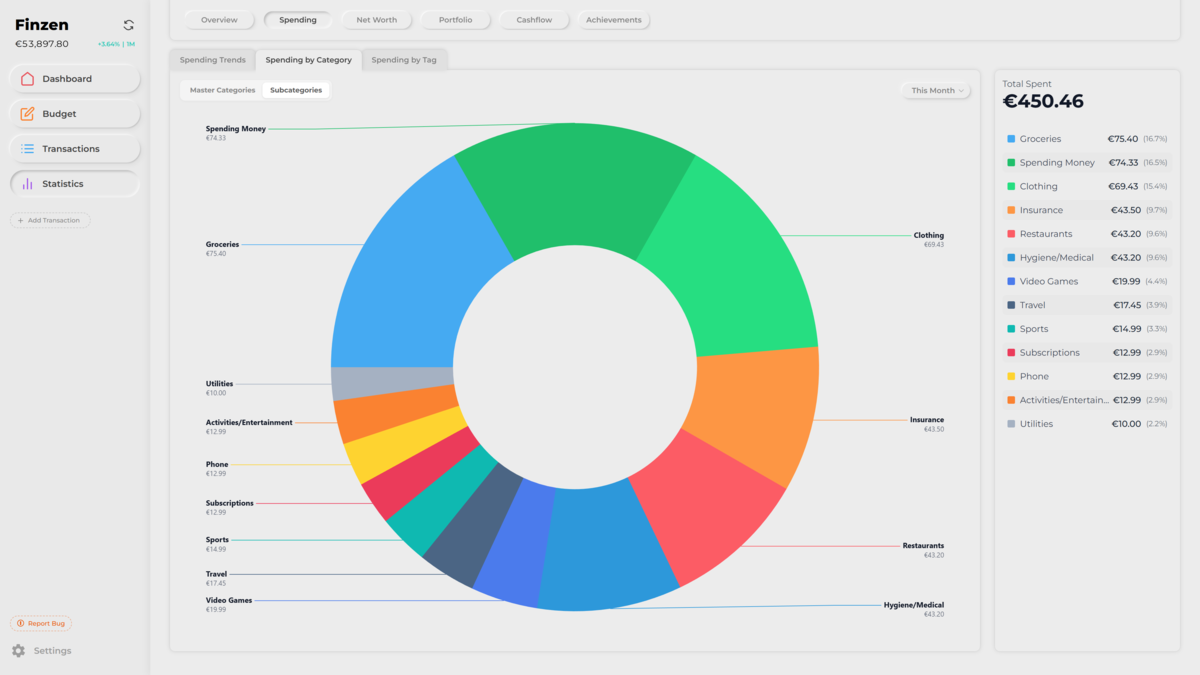

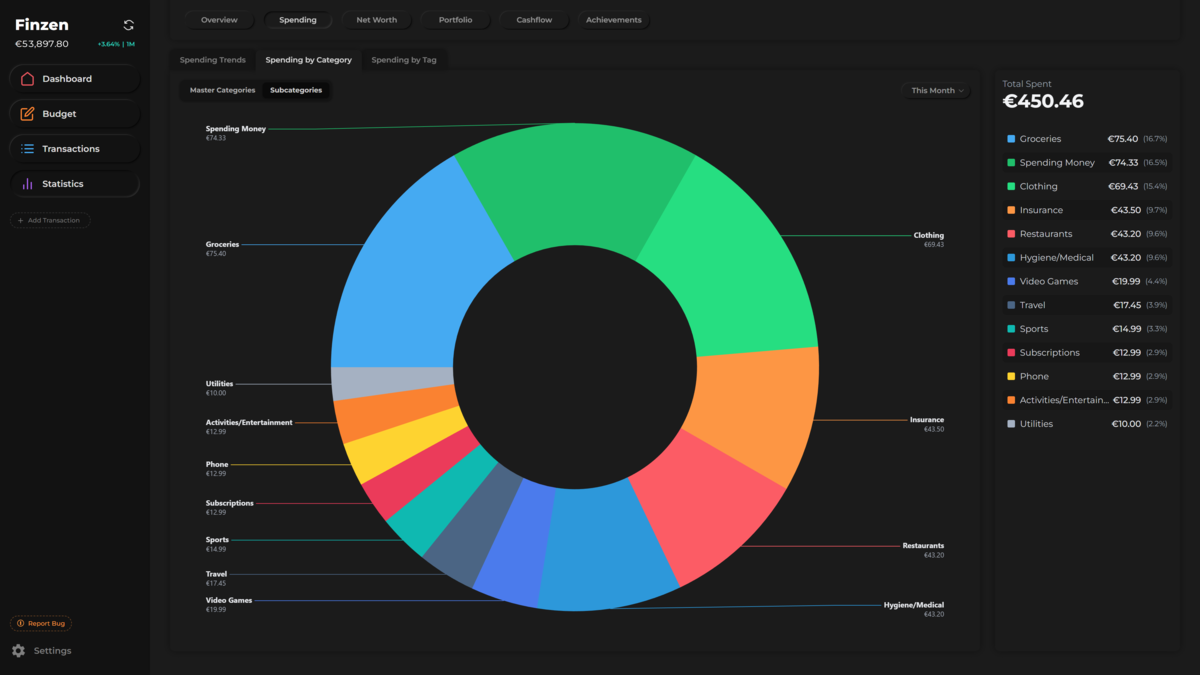

You've covered the essentials: budgeting, emergency funds, eliminating bad debt, and smart investing. Everything on this page lives in one place with Finzen - envelope budgeting to control spending, cash flow tracking to understand your runway, and portfolio management for every asset class from stocks to crypto.

No bank sync means your credentials stay private. Manual tracking in 2-3 minutes daily builds awareness that automation can't match - you see patterns, make better decisions, and stay connected to your finances. Budget, emergency cushion, and investments all visible together, showing exactly where you stand and what you can afford to invest.

If you want a simple tool that grows with you, give Finzen a try. It's free to start.

Continue exploring

Budget & Track Spending

Give every dollar a purpose. Set spending envelopes by category, log purchases as you go, and see your remaining budget update in real time.

The Finzen Method

Spend 2-3 minutes a day logging your expenses and you'll understand your money better than any bank sync ever could. No automation. Just awareness.

Charts, Reports & Insights

Log your spending, get the full picture. Daily entries become spending flows, budget charts, portfolio views, and a net worth timeline. All in one place.